Managing a deceased person’s estate frequently entails personal accountability, financial choices, and legal obligations. Executors must handle beneficiary pressure while properly allocating assets, paying off obligations, and abiding by the law. Knowing how to find probate insurance is a crucial step in estate administration because even a minor error can result in personal liability.

Understanding Probate Insurance and Its Purpose

The purpose of probate insurance is to shield administrators and executors from monetary losses brought on by inadvertent mistakes made when administering an estate. After assets have been distributed, these policies provide a safety net in case creditors or recipients file claims.

When executors are uncertain about possible unidentified debts or when estates are complicated, this coverage is extremely helpful. In the event of an unforeseen circumstance, options like executor insurance for estate administration offer confidence that personal resources won’t be at danger.

Who Should Consider Probate Insurance?

Probate insurance is advantageous for anyone serving as an administrator or executor. Family members, friends, or experts designated to oversee the estate fall under this category. Insurance gains even more value if the estate has foreign assets, unidentified liabilities, or absent beneficiaries.

Why It’s Important to Find the Right Probate Insurance

Selecting appropriate insurance is important for peace of mind as much as compliance. Even in cases where they act with good intentions, executors bear personal responsibility for their errors. People can move on with asset distribution with confidence and worry-free by obtaining probate insurance for executors.

Additionally, insurance keeps disagreements from getting worse. Reducing stress and delays, beneficiaries are reassured that financial support is available in case any problems subsequently emerge.

● Common Risks Faced by Executors

Claims against executors may arise from unpaid taxes, unidentified creditors, or inaccurate beneficiary identification. Only the executor’s personal cash may be used to settle these claims in the absence of coverage. These risks are considerably decreased by policies that provide estate administration insurance coverage in the UK.

How to Find Probate Insurance That Fits Your Needs

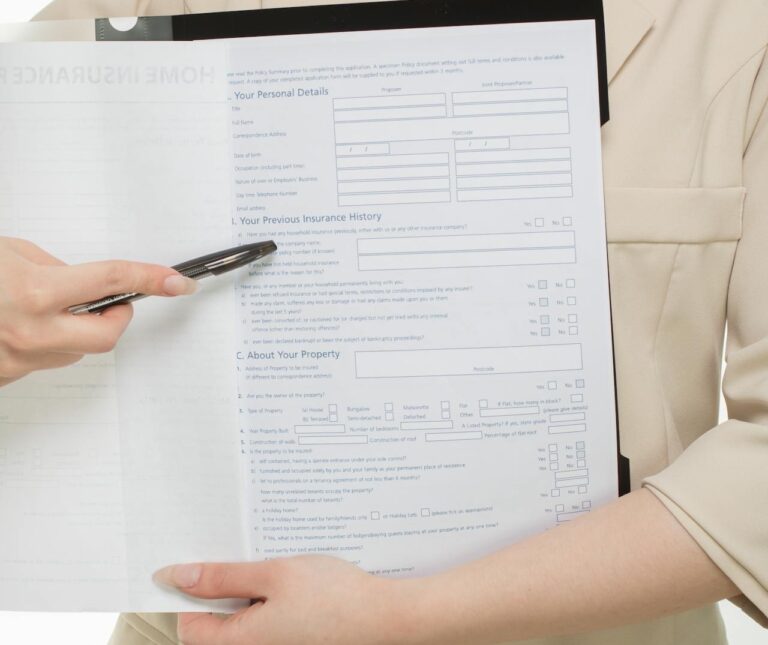

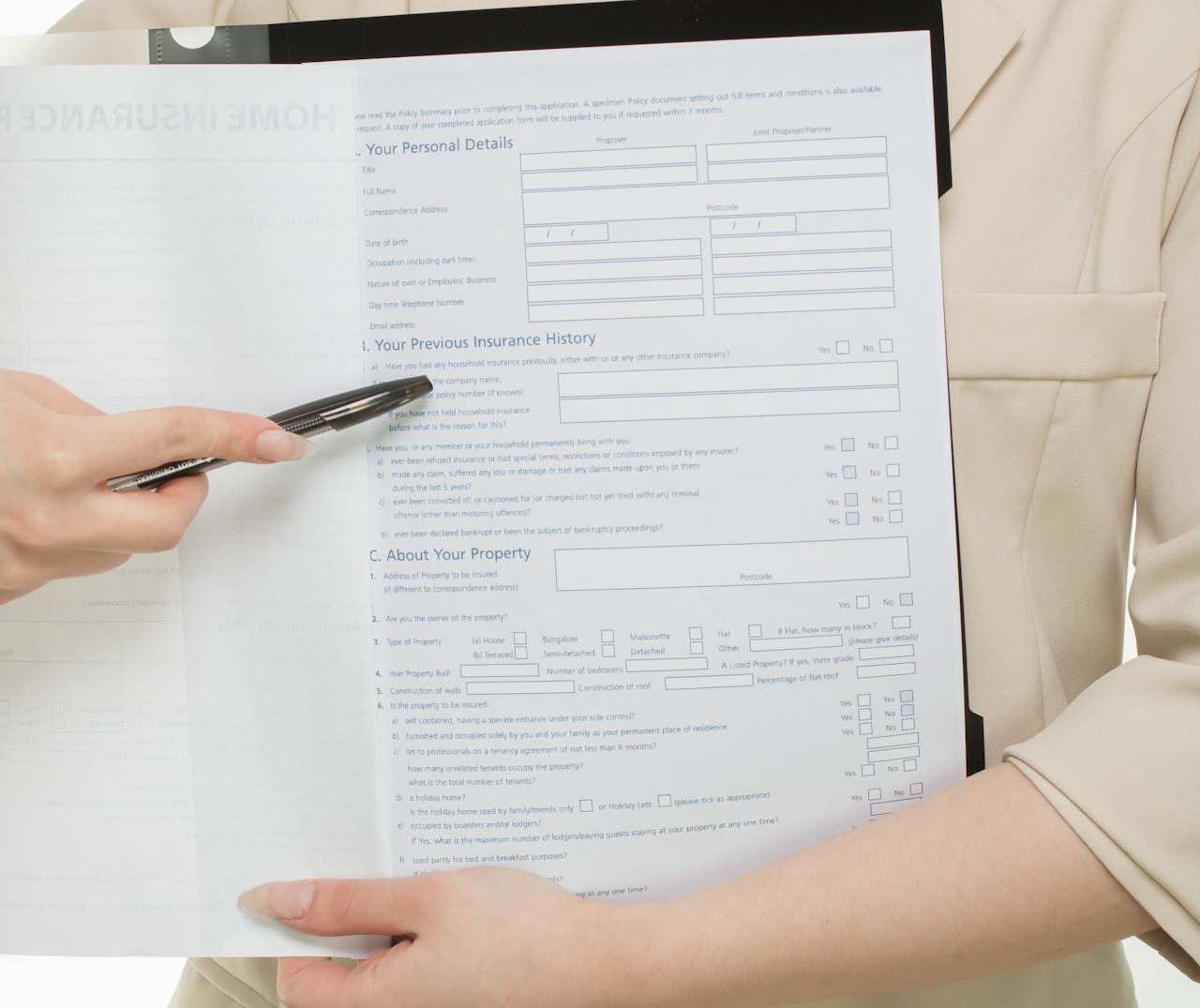

Knowing the size along with complexity of the estate is the first step in selecting the appropriate coverage. Potential hazards, such missing wills or contested assets, should be evaluated by executors. Usually, insurers need information regarding the sort of assets involved, the number of beneficiaries, and the estate value.

Selecting providers who specialise in legal and estate-related policies is advised. Probate-specific hazards are better understood by specialist insurers than by general insurance companies, which guarantees customised protection as opposed to generic coverage.

● What to Look for in a Provider

Crucial elements include openness, and precise policy language, as well as professional assistance. Seek out insurers who provide help during the probate procedure and provide clear explanations of exclusions. Options for coverage, such as protecting executors from liability, should be adaptable enough to accommodate various estate situations.

Benefits of Securing Probate Insurance Early

In order to assure continued estate administration, insurance should be arranged early in the probate process. It enables executors to take swift action without postponing distributions out of concern about possible claims. Additionally, early coverage shows prudent management, which can preserve beneficiaries’ trust.

Cost effectiveness is an additional benefit. Because there are less risks before distributions, early-arranged policies are frequently less expensive.

Also Read: Why Every Franchisee Needs a Franchise Lawyer Before Signing?

Conclusion

Finding probate insurance is a sensible first step toward managing an estate without worry. Before allocating estate assets, get the proper protection by visiting Insuristic today for professional advice and customised coverage alternatives.

FAQs

1. What does probate insurance cover?

Usually, it includes executor liability for mistakes, unidentified debts, or claims made after the distribution of the estate.

2. Is probate insurance legally required?

No, although shielding executors from personal financial risk is strongly advised.

3. Who pays for probate insurance?

The expense is typically covered by the estate rather than the executor’s personal funds.

4. Can probate insurance be arranged after distribution?

Certain insurance can, although there might be fewer and more costly options.

5. Does probate insurance delay the probate process?

No, it typically facilitates quicker decision-making and more efficient management.